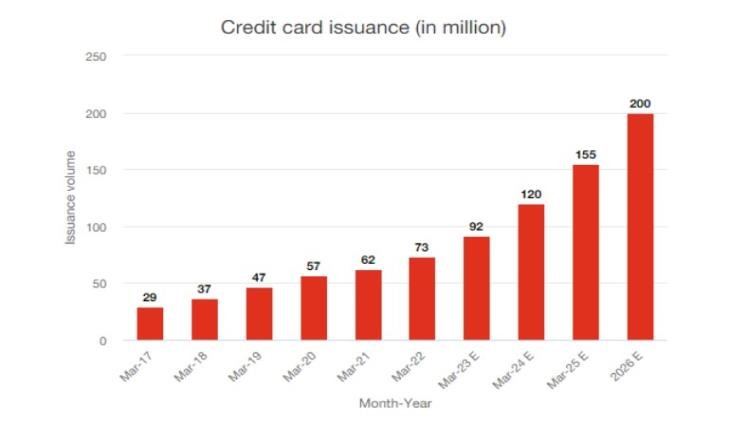

In India, credit cards are becoming immensely popular. Credit cards are designed to be both a payment method and a source of credit. The increased popularity of credit cards vis-à-vis other modes of payment could be understood by the fact that nearly 78 million credit cards were in use in India in July 2022.

Owing to the growing popularity of credit cards in India, credit card issuers are also launching a variety of innovative card products to make it easier for consumers to keep business and personal credit separate.

Sadly, a large number of people, especially small business and start-up owners often remain confused when it comes to business credit card vs. personal credit card.

Business Credit Card Vs. Personal Credit Card – What’s The Difference?

Personal credit cards, as their name suggests, are the types of credit cards intended for use by an individual or family for expenses such as food, entertainment, groceries, and other personal expenses. Business credit cards, on the other hand, are designed for usage by business owners and are largely used for covering business expenses.

What’s business Spend?

Ideally, a “business spend’” could be referred to as any expenditure that is specifically made for the business and not made for one’s personal needs or consumption. Business spending usually is a high-value expenditure made for managing one’s small business, start-up, or even a large enterprise.

Business Credit Card Vs. Personal Credit Card – 5 Mistakes You Should Avoid

Deciding between a business and personal credit card remains a daunting task for many. In fact, consumers frequently make mistakes without being aware of how it may affect their overall financial well-being.

And that’s why, in this article, we’ve listed down some typical mistakes that one should avoid when it comes to business credit card vs. personal credit card.

1: Using Your Personal Credit Card for Your Business Spends

Your personal CIBIL score is affected if you use your personal credit card to cover business spending. Remember, your personal credit score suffers if you are unable to pay off your credit card debt. When you ask for a loan for personal necessities, this will have an even greater impact on your loan eligibility. Depending on how low your credit score is, you may be required to pay exorbitant interest rates on loans, or you may not even be eligible for one at all. It then makes sense to avoid using your personal credit card for your business expenses. Instead, use business credit cards to cover all such expenses.

2: Missing out on the Higher Credit Limit Offered by Business Credit Cards

A business may need an enormous amount of money to pay for costly machinery and equipment, office renovations, lease payments, rent, and other business expenses. These expenses might add up to a substantial sum that may be challenging to pay for using a personal credit card. No matter how much credit you have available on your personal card, it will never compare to the credit available on a business credit card, which is built to meet the demands of a developing company. Therefore, carefully consider the credit limit when considering business credit card vs. personal credit card for your business.

- Losing on Business-Specific Rewards and Bonuses

Every type of credit card is specifically designed to provide you with a different set of offers to help you save money. By utilizing a personal credit card, you can, for instance, receive rewards when dining out, shopping, buying groceries, etc. A corporate credit card, on the other hand, will give you benefits like airline discounts, rewards on hotel reservations, business services, access to airport lounges, etc. These benefits might help your company cut costs across the board. Keeping the above point in mind, be very careful when considering business credit card vs. personal credit card for your business.

- Not Understanding the Need for Building Better Business Credit

You might be surprised to learn that 45% of small business owners are unaware of their business credit score. Remember, business owners with good business credit scores are more likely to be approved for a bank loan.

If you’re looking to apply for different types of business loans, equipment leasing, etc., you must have a business credit history. Additionally, investors, VCs, and lenders also investigate the business credit history of your company before authorizing any funds to assess risk and credibility.

If you use a personal credit card for business purposes, your credit history will be personal rather than business related. Resultantly, it will become challenging for you to get business loans, lease, and even raise capital for your business.

- Not Streamlining Employee Expenses

Remember, with personal credit cards, the customer sets their own spending restrictions. Most companies that issue credit cards for personal use let the user establish restrictions on where and how much money they can spend.

Business cards, on the other hand, can only be used for corporate expenses like travel, office supplies, etc., and come with spending limitations. This not only helps with budgeting and accounting, but it also saves time and effort for employee purchases. Employee cards provide for precise categorization rather than combining personal and business costs on one account.

Conclusion

In conclusion, both personal and business credit cards can be helpful financial instruments, but it’s crucial to recognize how they differ and to use them wisely. While personal credit cards help you access immediate purchase capability with a 45-day credit-free window, using business credit cards to make purchases and control the ups and downs of cash flow is a wise move for any company.

Business credit card vs. personal credit card, no matter what you choose for your business, it makes sense to avoid these mistakes to maximize the use of your credit card and reach your financial objectives.